Why the Bottom-Up Approach Works Better for Budgeting (And How to Use It)

The bottom-up approach to budgeting works better because teams build their own budgets based on real costs and needs. Most budgets start with leadership setting numbers, forcing teams to make them fit, even when they don’t match reality. This leads to bad forecasts, wasted money, and frustrated teams.

Bottom-up budgeting does the opposite. Teams create their own budgets, and finance turns those numbers into a plan that actually works. Forecasts improve, spending stays under control, and teams take ownership of their numbers.

Read: Strategic Financial Planning: How to Plan for Success

This guide covers how bottom-up budgeting works, why it leads to better results, and how to put it into action.

What Makes Bottom-Up Approach in Budgeting Unique?

Top-down budgets start with leadership setting limits. Teams then have to make the numbers work, even if they don’t match reality. The bottom-up approach does the opposite. Teams build their own budgets based on real costs and business needs. Finance then pulls everything together into a full company budget.

This keeps budgets accurate and flexible. Teams take responsibility for their numbers, which leads to smarter spending and better planning. Finance can adjust forecasts as needed instead of being locked into a plan that no longer makes sense.

Example: A manufacturing company applies the bottom-up approach by setting its budget for raw materials based on current production costs and demand, not last year’s numbers.

To make this work, teams need to track actual vs. planned spending. If numbers don’t add up, variance analysis helps catch the issue before it becomes a bigger problem.

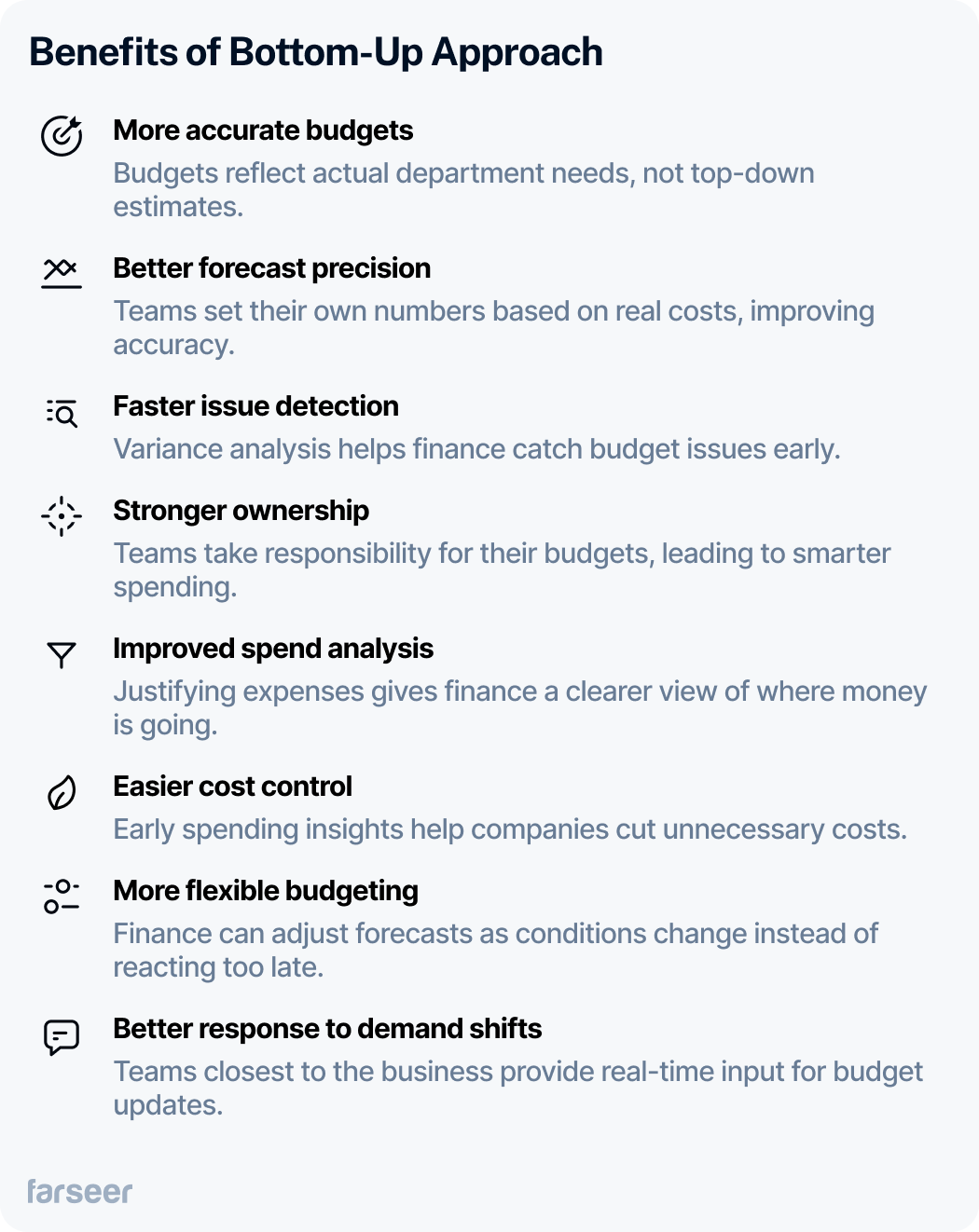

Why the Bottom-Up Approach Works Better

The bottom-up approach ensures a more accurate budget because it reflects actual department needs. Teams set their own numbers based on real costs, not leadership guesses. This improves forecast precision and helps finance catch issues early with variance analysis.

Teams also take ownership of their budgets, leading to smarter spending and fewer surprises. When they justify expenses, spend analysis improves, and finance gets better insight into where the money is going. With a clear breakdown of spending, it’s easier to spot unnecessary costs and adjust before they become a problem, which is why many companies rely on spend analysis to tighten financial control.

Bottom-up budgeting also makes it easier to adjust forecasts as conditions change. Instead of reacting too late, finance can tweak spending based on early indicators from the teams closest to the business.

Example: A retail company updates sales forecasts every quarter based on store data. If demand spikes, budgets adjust immediately instead of waiting for the next planning cycle.

Common Mistakes in Bottom-Up Approach in Budgeting (and How to Fix Them)

Over-Budgeting

Teams often inflate numbers to secure extra funding, assuming finance will cut their requests. This leads to bloated budgets and wasted resources.

Zero-based budgeting prevents this by requiring teams to justify every expense instead of copying last year’s numbers. This forces a detailed review of costs and keeps spending in check.

Example: A manufacturing company used zero-based budgeting and found supplier costs were higher than necessary. By renegotiating contracts, they lowered expenses without affecting production.

When departments focus only on their own needs, their budgets can drift away from company priorities. This leads to inefficient spending and missed financial targets.

Driver-based budgeting makes this easier by focusing on key cost drivers instead of checking every line item, ensuring that both operating expenses and capital investment plans align with business goals. By doing so, finance can spot budget requests that don’t match business priorities and make necessary adjustments early on.

Example: A financial services firm found that most new clients came from just two ad channels, yet its marketing budget was spread across multiple platforms. Refocusing on high-performing channels cut waste and improved acquisition.

Budgeting Takes Too Long

Gathering input from every team can drag on for weeks, delaying financial decisions and leading to outdated forecasts. A lack of standardized processes makes the problem worse.

Rolling forecasts and structured templates speed up the process and keep budgets adaptable throughout the year.

Example: A retail company’s budgeting process stalled because of inconsistent data formats from store managers. Standardizing templates and setting strict deadlines reduced budgeting time by 40%.

Many businesses use forecasting software to make this process faster and simpler.

Lack of Standardized Data

Without a consistent format, finance teams receive budgets full of conflicting numbers, assumptions, and reporting styles. This slows consolidation and increases errors.

A centralized budgeting system enforces reporting consistency and improves accuracy across departments.

Read more: Budget Management Software for Business: How to Finally Leave Excel Behind

Example: A healthcare company struggled with mismatched budget submissions across multiple locations. After implementing a standardized system, errors dropped, and financial reporting became more reliable.

Standardized reporting also makes comparative balance sheet analysis easier.

Ignoring Cost Drivers

Budgets based only on historical expenses often miss the real drivers behind costs, leading to inaccurate projections.

Cost-volume-profit (CVP) analysis helps finance teams understand what actually impacts profitability and adjust spending accordingly.

Example: A logistics company noticed rising transportation costs but hadn’t accounted for fuel price changes. After introducing CVP analysis, they adjusted spending based on real-time cost drivers.

Inconsistent Budget Reviews

Many teams submit budgets once a year and never revisit them, causing outdated forecasts and unnecessary spending. Without regular budget reviews, inefficiencies go unnoticed.

Setting up quarterly reviews helps finance catch cost overruns early and make necessary adjustments.

Example: A software company reduced costs by eliminating unused subscriptions after introducing quarterly budget reviews.

Companies that regularly track profit margins during budget reviews make smarter financial decisions and keep spending under control.

Learn more about margin analysis and how it helps businesses improve cost control.

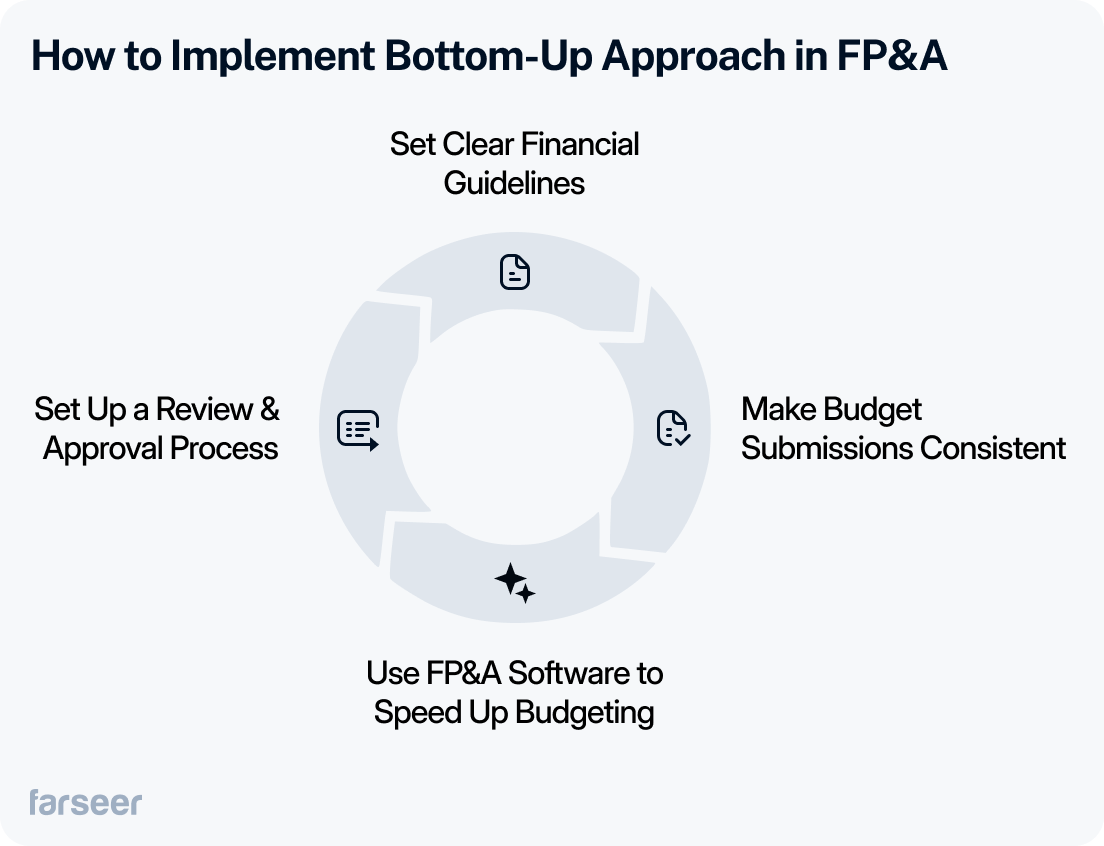

How to Implement Bottom-Up Approach in FP&A

Step 1: Set Clear Financial Guidelines

Teams need a starting point before they begin budgeting. If leadership doesn’t set clear financial targets, departments work in silos, making guesses that don’t always support company goals.

Before budgeting starts, leadership should:

- Define priorities – Where should the company invest more? Where should it cut back?

- Set financial limits – How much should each department plan for based on revenue goals?

- Align with strategy – Budgets need to match business growth plans, not just last year’s numbers

Companies shifting from top-down to bottom-up budgeting often struggle with this step because teams aren’t used to setting their own financial plans. Establishing clear guidelines makes the transition smoother and keeps budgets aligned with company goals. Learn more about how to move from top-down to bottom-up budgeting.

Example: A manufacturing company planned to expand production, but individual teams didn’t know that upfront. Once leadership set growth as a priority, department budgets focused on efficiency instead of unnecessary cost-cutting.

Step 2: Make Budget Submissions Consistent

If every department submits budgets in a different format, finance has to waste time fixing errors instead of focusing on the numbers. Messy, inconsistent data makes it harder to compare budgets, slows everything down, and leads to mistakes.

A simple budgeting template solves this. When every team follows the same format, finance can easily review and combine numbers. Tracking past budgets also helps spot patterns – like teams always asking for more than they spend, so forecasts get more accurate over time.

Example: A healthcare company had a budgeting mess with different locations using their own spreadsheets. After switching to a standard format, budget reviews took half the time, and finance caught errors before they became bigger problems.

Step 3: Use FP&A Software to Speed Up Budgeting

Chasing down spreadsheets from every department takes forever and leads to mistakes. By the time finance puts everything together, the numbers are outdated, and teams have already moved on.

FP&A software fixes this by pulling in budget data automatically. Finance can track changes in real time, catch errors early, and adjust forecasts as needed – without waiting weeks for final numbers.

Example: A logistics company kept running into last-minute budget changes that threw off planning. After switching to an FP&A tool, they could see department budgets update live, so they made smarter spending decisions without scrambling at the end.

Step 4: Set Up a Review & Approval Process

A budget draft isn’t the final version. Without a proper review, teams overestimate needs, and finance might approve spending that doesn’t fit company goals.

A tiered approval process fixes this. Before finance finalizes the budget, leadership should review department requests, flag unrealistic numbers, and cut unnecessary spending. This is especially important when making decisions about CapEx vs. OpEx, as long-term investments require different approval workflows than day-to-day operational costs.

Driver-based budgeting makes this easier by focusing on key cost drivers instead of checking every line item. This helps finance spot budget requests that don’t match business priorities.

Example: A logistics company added a tiered review and cut 10% in unnecessary costs by flagging spending that didn’t support revenue goals.

Bottom-Up Approach - Key Takeaways

- Bottom-up budgeting makes forecasts more accurate because teams use real costs, not top-down estimates.

- Teams take responsibility for their budgets, which leads to smarter spending and fewer surprises.

- Clear financial guidelines and regular reviews keep budgets aligned with company goals.

- Tracking the right metrics helps finance catch issues early and adjust as needed.

- A structured approval process keeps budgets realistic and focused on what matters.

Companies that switch to bottom-up approach gain better control, improve spending decisions, and stay flexible as business conditions change. If your budgeting process is slow, full of guesswork, or disconnected from reality, adopting the bottom-up approach can bring more accuracy and control.Give teams control over their numbers while keeping finance in the driver’s seat.

Budget Forecasting Methods: 6 Approaches Every CFO Should Know (And How to Choose)

Read more

Strategic Financial Planning That Actually Drives Results

Read more