What is Direct Cash Flow Method and When to Use It

The cash flow statement is one of 3 pillars of every financial system within a company, next to the income statement and balance sheet. But unlike the income statement, the cash flow statement focuses only on actual cash transactions. Why is this important?

Cash flow is the best measure of a company’s liquidity. It shows whether a business generates enough money to cover its obligations, finance operations and invest in growth. And this definitely is a crucial factor in assessing a company’s financial health.

There are two primary methods for calculating cash flow from operating activities: the direct method and the indirect method. Both of them offer unique insights, but the direct method makes it much easier to track cash activities. How? Let’s find out.

What’s a Direct Cash Flow Method

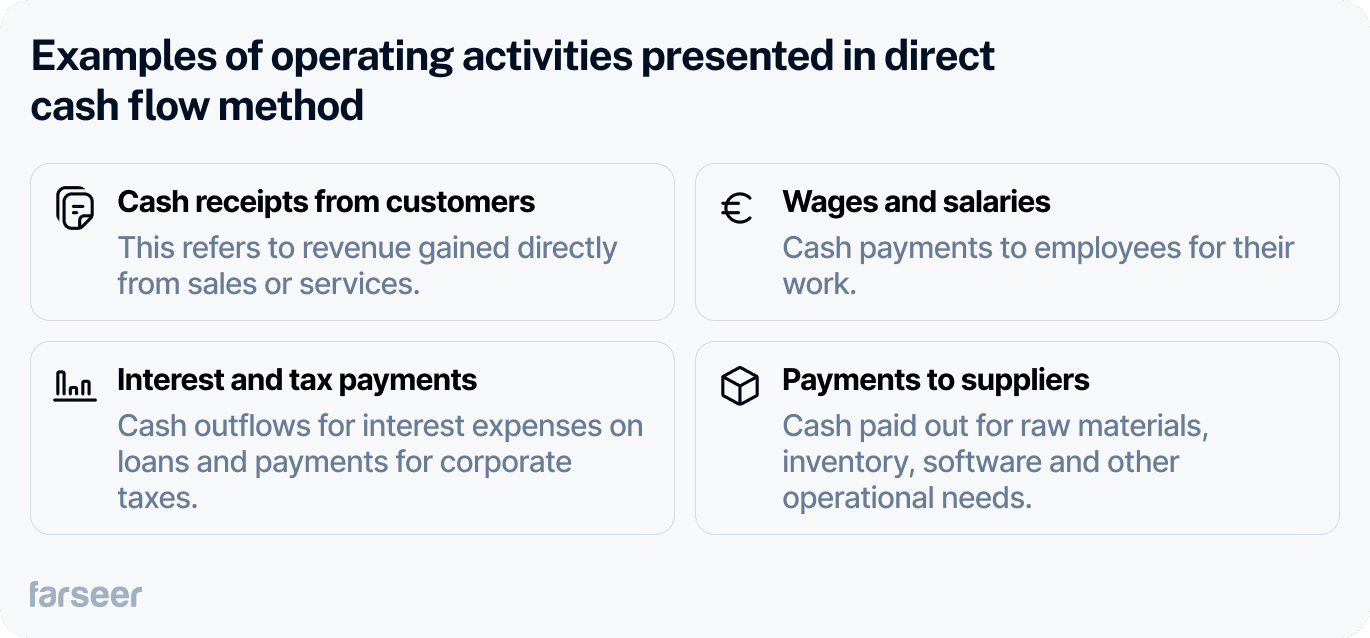

The direct cash flow method provides a rather simple approach if you need to calculate cash flow from operating activities, like receipts from sales, employee salaries, tax payments, etc. Unlike the indirect method, which begins with net income and adjusts for non-cash items, the direct method breaks down each cash transaction. This allows businesses to track cash inflows and outflows in detail, offering a clearer, more detailed view of what happens with cash day-to-day.

In the direct method, cash flows from operating activities are calculated by summarizing specific types of cash transactions, such as:

These direct cash flow details make it easy to see where and how cash is generated and spent. As such it offers a transparent view of finances which is a great basis for financial analysis and decision-making and ultimately, it shows if a company’s operations run in a healthy way.

Read: Cash Ratio Definition – A Simple Guide to Liquidity + Examples

Advantages and Disadvantages of Direct Cash Flow Method

The direct cash flow method has numerous advantages that make it an extremely valuable tool for businesses and analysts, but it also comes with some challenges. Let’s look at both sides.

Advantages of direct cash flow method

A clearer and more precise image of cash inflows and outflows

Since it lists all cash transactions related to operating activities, the direct method presents clearly where cash is coming from and where it’s going.

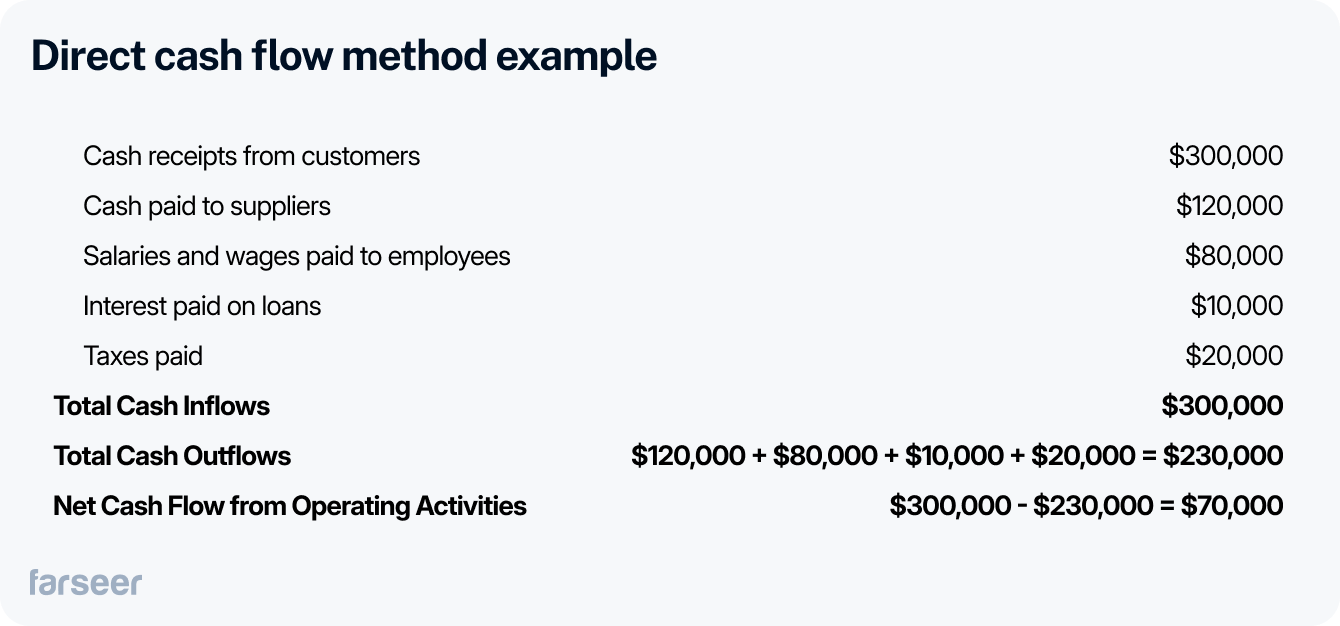

Imagine a company using this method of cash flow. Their cash flow statement may look something like this:

In this example, the direct method breaks down each source of cash inflow and each type of cash outflow individually. The net cash flow from operating activities can then be calculated by summing these transactions.

This format offers a clear view of where cash is coming from (customers) and where it is being spent (suppliers, employees, interest, and taxes). This helps businesses make precise financial decisions. For example, to identify areas where cost can be reduced or to understand how cash is generated from core operations.

Read: Consolidated Cash Flow Statement: Definition, Example, and Modern Approach

Better insights for stakeholders

This transparency is crucial for investors and managers because they easily identify cash-generating and cash-consuming activities.

Consider a manufacturing company that uses the direct method for its cash flow statement. For a specific quarter, the cash flow statement might look like this:

- Cash received from customers: $600,000

- Cash paid for raw materials: $250,000

- Salaries and wages paid to employees: $150,000

- Maintenance and equipment repair expenses: $30,000

- Rent for warehouse space: $20,000

- Utilities and other operational costs: $10,000

From this breakdown, stakeholders get a clear picture of:

- Cash-generating activities: The $600,000 received from customers shows the revenue generated by selling products.

- Cash-consuming activities: Each type of expense is listed, so it’s easy to see that raw materials ($250,000) and salaries ($150,000) are the biggest outflows, with other costs like maintenance, rent, and utilities also reducing cash.

With this visibility, managers can identify areas where they can optimize the costs, like negotiating with suppliers to lower raw material costs. Investors can assess whether cash-generating activities (like customer sales) are strong enough to cover operating expenses. And this is a key factor in deciding whether to continue supporting or investing in the company.

Disadvantages of direct cash flow method

It requires detailed data

The direct method requires companies to have detailed records of all cash transactions. This can be time-consuming and complex to track, especially for larger organizations.

Think of a large retail chain with thousands of daily cash transactions on multiple locations. To prepare a cash flow statement using the direct method, the company would need to list all cash movements like:

- Daily cash receipts from customers in each store and from online sales, which could require hundreds of thousands of entries monthly.

- Cash paid to each supplier for inventory restocking, which includes hundreds of invoices across various categories.

- Cash payments for employee wages, rent for each store, utility bills, and other operating expenses like marketing, cleaning services, equipment maintenance, etc.

Tracking each transaction separately would mean that the company’s accounting team has to gather and categorize each payment, receipt, and cash outflow individually. For a large organization, this can be really complex. Additionally, it would require sophisticated accounting systems and possibly additional staff to make sure that every transaction is recorded in the right way.

For instance, if this retail chain has 100 locations and each location 500 transactions a day on average, this would result in 50,000 daily entries just for customer cash receipts. If you add inventory purchases, wages, and other expenses, you can imagine the amount of data and data management systems it would require. This often leads larger companies to choose the indirect method just because it’s a simpler way of cash flow reporting.

Less common in reporting

The indirect method is more widely accepted, especially under U.S. Generally Accepted Accounting Principles (GAAP). GAAP allows both methods, but companies using the direct method are often required to adjust their statements by also providing an indirect cash flow calculation. This additional step can make reporting more complex, which is why most companies opt for the indirect method by default.

Why the indirect method is more common

Under the indirect method, companies start with net income from the income statement and adjust it for non-cash items and changes in working capital to calculate cash flow from operations. Since companies already calculate net income, this method is easier to implement and doesn’t require detailed tracking of every transaction, so it’s quite obvious why many companies opt for this method.

Imagine a company that decides to use the direct method for its cash flow statement. It provides a detailed breakdown of cash inflows and outflows, however, because this approach is less common, U.S. GAAP requires the company to also present an adjustment to the indirect method.

This adjustment would involve:

- Starting with net income from the income statement.

- Adjusting for non-cash expenses like depreciation.

- Accounting for changes in working capital, such as increases or decreases in accounts receivable and payable.

By providing both views, the company ensures its financials are compliant with GAAP but ends up doing twice the work. For many companies, this requirement makes the direct method less appealing, because the added step is time-consuming and unnecessary, despite all its benefits.

Conclusion

The direct cash flow method gives financial professionals a clear look at day-to-day cash activities, even though it needs more detailed data than the indirect method. Choosing between the two methods depends on a company’s reporting needs, regulatory rules, and the level of detail wanted. Understanding both methods helps businesses create cash flow statements that match their financial goals and meet any reporting requirements.

To make the process easier, you can start with this ready-made monthly cash flow Excel template, structured for real-world planning and versioning.

Financial Statement Analysis: The Complete Guide (With Step-by-Step Process)

Read more

Best Financial Analysis Tools in 2026: Compare Features & Pricing

Read more