Consolidation vs equity method? How to choose which one is for you?

Financial reporting gets complicated the moment your company expands beyond a single legal entity. Subsidiaries, joint ventures, strategic stakes… Each structure triggers different accounting rules. And the method you choose doesn’t just affect compliance. It shapes how your performance, risk, leverage, and profitability are presented to leadership and external stakeholders.

Read Financial Consolidation: Definition, Challenges & Solutions

Two methods dominate group reporting: consolidation and the equity method. Both are correct, but they serve very different purposes.

This guide breaks them down in plain language so you can assess best which one aligns with your ownership structure, level of control, and reporting goals.

The Core Difference Between Consolidation and Equity Method

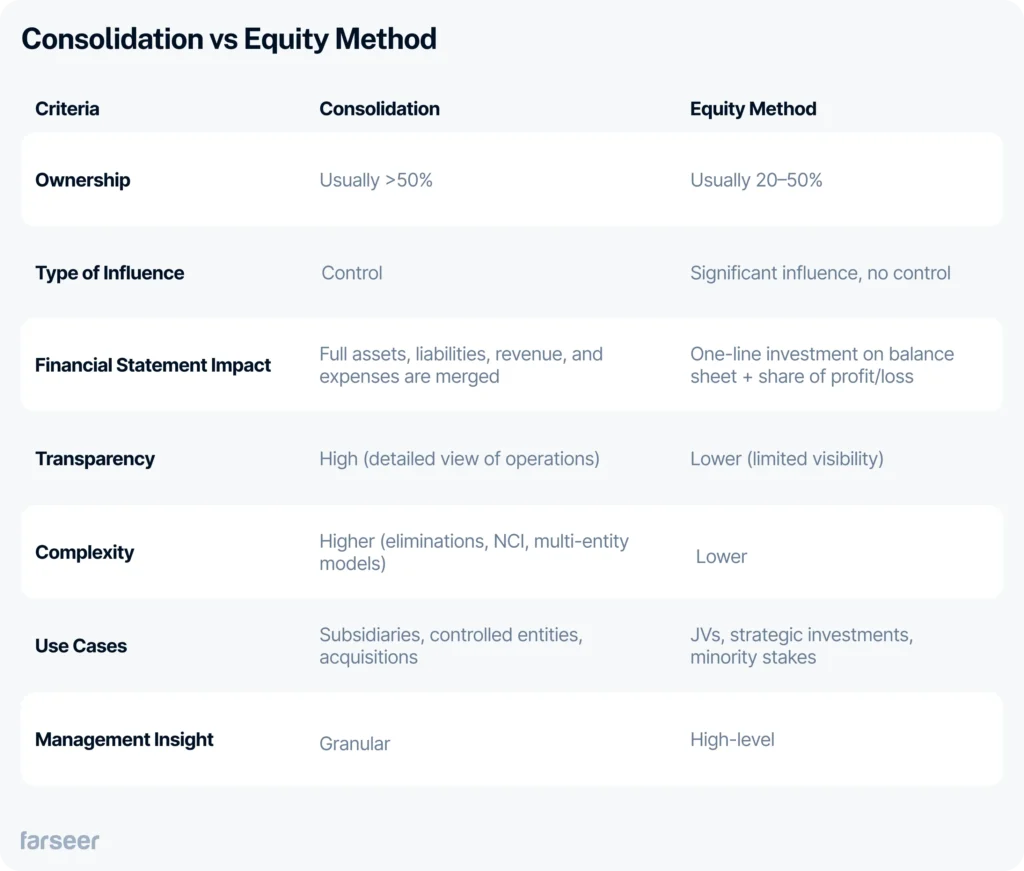

To put it in simple terms: With consolidation, you’re in full control, so you combine everything and report as one company. With the equity method, you don’t run the show, but you have influence, so you only report your share of the profit or loss.

If you remember nothing else, remember this.

Let’s dig a little deeper.

When to Use Consolidation

Consolidation is required when a company controls another entity. Under IFRS 10, “control” means:

- Power over the investee

- Exposure to variable returns

- Ability to use power to affect returns

Most often, this looks like ownership above 50%, but percentages alone don’t tell the whole story. Board rights, veto rights, and governance structures can create control even at lower ownership.

Read Best Consolidation Software in 2025: Top Tools, Key Features, and How to Choose

What consolidation looks like in practice

In real life, consolidation basically means you’re treating your subsidiary’s books as an extension of your own. Everything they have, do, owe, or earn gets pulled into your financials.

That means all their assets and liabilities, all their revenue and expenses, and even their cash flows – everything gets merged line by line, as if the two companies were one.

After that, you tidy things up:

- Any transactions between you and the subsidiary get eliminated (otherwise you’d be counting them twice).

- And if you don’t fully own the subsidiary, you show the portion that belongs to other shareholders as non-controlling interest (NCI)

It’s a bit of work, but the result is a clean, complete picture of the entire group.

Why businesses use consolidation

It gives a full picture of:

- Total group performance

- Cash position and liquidity across entities

- Exposure to debt, FX, and operational risk

- Group-wide margins and profitability

- Resource allocation and CAPEX planning

If you’re running a parent company with subsidiaries – whether in pharma, manufacturing, distribution, or retail – consolidation is the only method that reflects the reality of group control.

When to Use the Equity Method

The equity method is used when you have significant influence, but not full control.

This typically means 20–50% ownership, but again, real influence matters more than percentages.

Examples:

- A 30% stake in a distribution partner

- A joint venture (JV) for R&D

- A strategic investment in a related operation

What the equity method looks like

With the equity method, things are much simpler, almost minimalist.

Instead of pulling in the entire financials of the other company, you just show one line on your balance sheet that represents your investment. That’s it.

Then, each period, you adjust that line based on your share of their profit or loss. So if your joint venture makes €10M and you own 30%, you book €3M. If they take a loss, your investment goes down accordingly.

And here’s the key part: You don’t merge their revenue, their expenses, their assets, or their liabilities into your statements. All of that stays in their own books. You simply reflect your economic stake, not their full operations.

It’s a clean way to show, “We’re involved, but we’re not running the place.”

Why businesses use the equity method

It’s ideal when:

- You’re involved strategically, but not running operations

- Your stake affects financial outcomes but not daily decisions

- You need visibility into economic performance without full integration

It simplifies reporting compared to consolidation, but also hides operational detail, which can be a challenge for planning and forecasting.

Read Pecking Order Theory: Definition, Examples & Applications

How Modern Planning Platforms Handle Both

Today’s multi-entity groups don’t have the patience, or the time, to wrestle with endless spreadsheets just to get a clear picture of their numbers. They want real-time reporting, clean ownership logic, and results that update the moment something changes.

This is exactly where modern FP&A platforms (like Farseer) change the game.

They take care of the heavy lifting automatically:

- Ownership rules apply themselves – no more hunting through formulas to see where 60/40 splits went wrong.

- Both consolidation and the equity method live inside one governed model, so you’re not juggling separate files or manually stitching reports together.

- Results update instantly whenever ownership percentages shift or a JV’s performance changes.

- Eliminations and NCI? Handled for you, so the group view is always accurate.

- All the logic stays fully traceable for audits, regulators, and anyone who wants to understand how numbers came to be.

- And when you want to run scenarios, e.g. “What if we increase our stake?” “What if the JV underperforms?”, you can model them without cloning spreadsheets or creating version chaos.

This is where connected, governed models really shine.

Compared to Excel, which quickly becomes a maze once you’re dealing with multiple entities or cross-border structures, modern platforms keep everything consistent, transparent, and fast.

Exactly what growing finance teams need.

Which Method to Choose

Choosing between consolidation and the equity method is actually a visibility and control decision.

- If you run operations – consolidate.

- If you influence, but don’t control – equity method.

- If you need transparency and forecast accuracy – choose systems that support both.

A clear understanding of ownership, influence, and reporting requirements ensures your financial statements reflect reality, and your decisions are based on trustworthy data.